The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP17 Grow With the Book You Already Own

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

📝 Episode Description

In this episode of The Insurance Producers Guild, we break down a major 2026 growth opportunity for Medicare agents: the book of business they already own.

With lead costs rising and acquisition economics getting tighter, buying more leads is not always the best path to profitable growth. Meanwhile, LIMRA reports continued strength in life insurance, annuities, IUL, and RILAs, while Corebridge Financial and Greenwald Research show growing consumer interest in guaranteed retirement income.

This episode shows agents how to audit their existing CRM, identify cross-sell opportunities, and turn annual reviews into practical conversations.

🔑 Key Topics Covered

Rising lead costs and acquisition pressure

Why your existing book may be the better growth play

2026 life insurance and annuity trends

Retirement-income demand from today’s clients

How to segment your book for cross-sell opportunities

A simple annual-review outreach script

🎯 What This Means for Agents

Existing clients may be your strongest 2026 growth asset

Rising acquisition costs make reviews more important

Clients are already asking about income and protection

Annual reviews create natural cross-sell conversations

CRM audits can uncover faster, more profitable growth

📌 GO-DO

This Week: 24–48 Hours

Export your Medicare client list from your CRM and tag every client with one of three flags:

- Over 62 with retirement assets

Annuity or RILA conversation prospect - Still working, pre-Medicare

IUL or needs-analysis prospect - Medicare client with adult children

Life insurance referral prospect

Infographic: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP17_Infographic.png

{kind=link}

Slides: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP17_Slides.pdf

🔗 Sources

LIMRA — U.S. Annuity Sales Notch Tenth Consecutive $100 Billion Quarter

https://www.limra.com/en/newsroom/news-releases/2026/limra-u.s.-annuity-sales-notch-tenth-consecutive-%24100-billion-quarter/

LIMRA — U.S. Individual Life Insurance Sales Show Strong First Quarter Growth

https://www.limra.com/en/newsroom/news-releases/2026/limra-u.s.-individual-life-insurance-sales-show-strong-first-quarter-growth/

Corebridge Financial / Greenwald Research — Decumulation Study

https://www.corebridgefinancial.com/insights-education/decumulation-study

Corebridge Financial — Only 28% of Pre-retirees and Retirees Are Comfortable Drawing Down Savings in Retirement

https://investors.corebridgefinancial.com/news/news-details/2026/Only-28-of-Pre-retirees-and-Retirees-are-Comfortable-Drawing-Down-Savings-in-Retirement-But-Having-a-Plan-for-Decumulation-Boosts-Confidence/default.aspx

PSM Brokerage — Medicare Lead Generation and Agent Marketing Resources

https://www.psmbrokerage.com/14-ways-to-generate-medicare-leads

Kadence 2026 Report

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

So you are staring at the ceiling at two in the morning. Um, you are running harder than you ever have, you are dialing until your fingers are numb.

SPEAKER_01Right. And you are paying more for every single lead, you know?

SPEAKER_00Exactly. And despite all that hustle, your agency just feels completely stuck in neutral. It is like, well, it feels like you are sprinting on a treadmill that just keeps speeding up.

SPEAKER_01That is the exact nightmare keeping independent agents awake right now. The pressure is just suffocating. You feel like if you stop buying leads for even one week, your entire pipeline is gonna collapse.

SPEAKER_00Yeah, I have been through this cycle before. I have seen the patterns across thousands of agencies. But we are going to start our exploration of the sources today with a reality check that will actually help you sleep tonight. The fastest growth lever for your agency in 2026 is not another expensive lead source. No. It is not some magic new marketing funnel.

SPEAKER_01Definitely not. The growth you are desperately looking for is already sitting in your CRM. I mean, you have already paid for it. The hardest part of the job, which is earning a client's trust, is already done.

SPEAKER_00Welcome to the Insurance Producers Guild by PSM Brokerage. We have a huge stack of data today from Cadence, Limera, and Corebridge. Our mission is incredibly simple. We are going to prove to you that every Medicare only client in your book is a warm cross cell waiting to happen.

SPEAKER_01Yes.

SPEAKER_00And we're going to walk through the exact field-tested scripts to monetize them this week.

SPEAKER_01Let us get right into the math because um, before you can grow, you have to stop the bleeding.

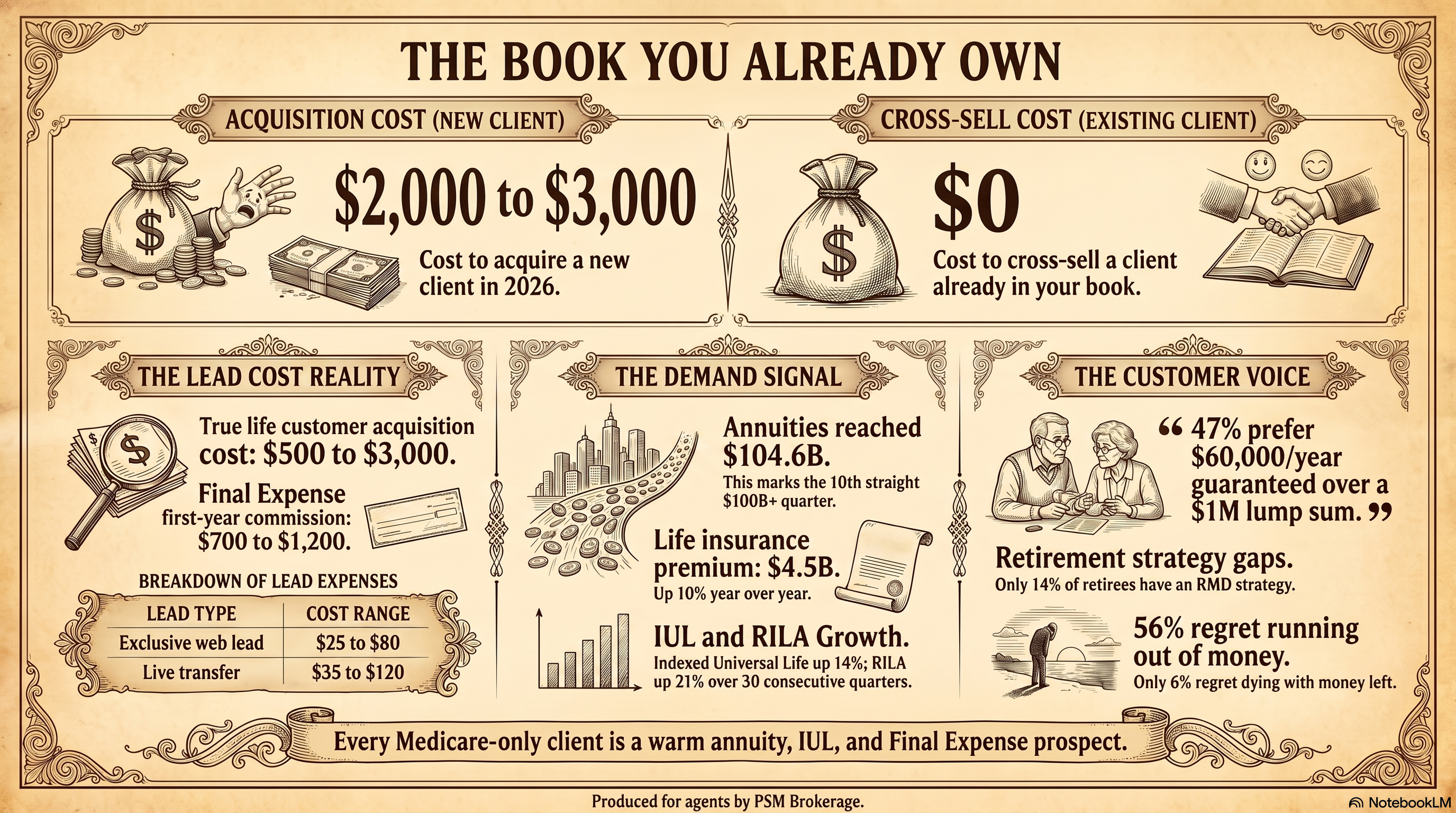

SPEAKER_00Exactly. I look at the market right now and I see a structural crisis. Chasing volume with new leads is a mathematical trap. We have the Cadence 2026 AI Creative Testing Data Report right here, and the numbers are honestly terrifying. Lead costs are absolutely surging.

SPEAKER_01Surging might be an understatement, honestly.

SPEAKER_00Right. Aged final expense leads are running $1 to $15. Facebook and social leads are $12 to $30. Shared web leads, which we know get sold to five different agents anyway, are $15 to $35.

SPEAKER_01Wow.

SPEAKER_00And if you want exclusive web leads, you're looking at $25 to $80 or more. Live call transfers are hitting $35 to $120.

SPEAKER_01Aaron Powell Which sounds painful just hearing the list. But the real problem is that agents confuse the cost of a lead with the true customer acquisition cost. They are not the same thing.

SPEAKER_00Break that down for us. What is the actual difference?

SPEAKER_01Well, the cost of a lead is just the price of a phone number. The customer acquisition cost, or PAC, is what it actually costs your business to put a new policy holder on the books. You have to factor in the labor of calling them 20 times. Right. You have to factor in your CRM software costs. Most importantly, you have to factor in the 20 bad leads you bought just to find the one person who actually picked up the phone and bought a policy.

SPEAKER_00And the data on that true cost is sobering. According to the data, true acquisition cost for life insurance now sits between $500 and $1,500 per policy holder. Elite RT estimates that number is even higher. They put the true cost at $2,000 to $3,000 per client.

SPEAKER_01And this is where the math really falls apart for the independent agent.

SPEAKER_00Here is the pattern I am seeing. If your true acquisition cost on a new prospect is $2,000, but your first year final expense commission is only $700 to $1,200, you are buying a loss. You are structurally underwater from day one. Exactly. You are filling a leaky bucket, crossing your fingers, and praying for renewals in year two just to break even. Small books simply cannot survive that math.

SPEAKER_01The instinct for most agents is to just buy a cheaper lead list to make up for the losses. You know, they think volume will save them. That is a wrong move. My advice to you right now is this do not spend another dime on leads today. Stop entirely. Audit your CRM first.

SPEAKER_00Wait, hold on. Turn off the lid flow completely. If I tell an independent agent to turn off their leads today, they are going to panic. They have rent to pay, they have carrier minimums to hit. How do they keep the lights on this month if they just stop prospecting?

SPEAKER_01Well, they do not stop prospecting. They just stop prospecting cold strangers. Think about it. If you already have 200 or 500 clients in your CRM whose acquisition cost you already paid three years ago, the highest ROI growth move is selling another product to the book you already own. Every Medicare only client you have is a warm prospect who already trusts you, and they cost you zero dollars to reach today.

SPEAKER_00Okay, I see your point. But what if an agent still wants to run ads?

SPEAKER_01Then use your CRM for that too. The data shows that first party look-alike audiences see conversion rates three to five times higher than broad targeting.

SPEAKER_00Let's clarify that term for a second. First party look-alike audiences. That sounds like um high-level marketing jargon. What does that actually mean for a solo producer?

SPEAKER_01It means you take a list of your best current clients from your CRM, you upload that list to a platform like Facebook. The algorithm then goes out and finds new people who share the exact same data points, behaviors, and demographics as your best clients.

SPEAKER_00Oh wow.

SPEAKER_01Yeah. You are essentially asking the system to find twins of the people who already buy from you. It is incredibly efficient.

SPEAKER_00But calculating those true acquisition costs to begin with can be tricky. Some agents might not even realize they are underwater because they only look at the commission check, not the blended cost of their marketing.

SPEAKER_01That is where verified support changes the game. If you are struggling to calculate your true customer acquisition costs and figure out your actual margins, this is where PSM brokerage's verified business coaching really proves its value. Right. They will sit down and help you map out your profitability metrics so you know exactly where you are losing money and where you are making it.

SPEAKER_00So you have stopped buying bad leads. You know your margins, you are looking at your CRM. The next step is understanding what your existing clients actually want to buy right now. I have been watching the LemRai Q1 2026 numbers, and the pattern is impossible to ignore.

SPEAKER_01Definitely.

SPEAKER_00There is a massive shift happening in consumer demand.

SPEAKER_01Aaron Ross Powell The demand is absolutely staggering. We are seeing numbers that redefine the market completely.

SPEAKER_00Let us look at the facts. Life premium hit $4.5 billion in the first quarter, which is up 10% year over year. That is well above LIMRA's full year forecast of 2-6% growth.

SPEAKER_01Right.

SPEAKER_00And policy count rose 9%. That means more Americans are buying coverage, not just wealthier ones buying bigger policies.

SPEAKER_01Aaron Powell And annuities are maintaining incredible strength, you know. Total U.S. annuity sales reached $16 billion in Q1. That is the tenth consecutive quarter over the $100 billion mark. Limeray says this $100 billion level has stabilized as a new normal. It is not a fluke anymore.

SPEAKER_00Aaron Powell And look at the specific products driving this. Index Universal Life, or IUL, is up 14%. It now makes up a quarter of all new annualized premium. Yeah. Registered index linked annuities, or ILAs, are up 21% to $21.2 billion. That is the second best quarter on record and the 30th consecutive quarter of year-over-year growth. This is a massive sustained wave.

SPEAKER_01We need to explain why those specific products are surging, though. What do an IUL and RELA actually do for a client?

SPEAKER_00Simply put, they offer participation in the market's upside, but they protect against the downside. An IUL uses index options to credit interest. So if the market crashes, you do not lose your principal. Right. RLA offers a buffer. The insurance company absorbs the first 10 or 20% of market losses. They are tools built for downside protection.

SPEAKER_01Exactly. And the psychology behind this surge is fascinating. It is not just about elevated interest rates, although those certainly help the product illustrations. We know exactly why this is happening because the Corbridge and Greenwald Research Decumulation Planning Gap Study spells it out perfectly.

SPEAKER_00Aaron Powell Right, the decumulation study.

SPEAKER_01Yeah. They surveyed 2,210 adults aged 45 to 79 with $100,000 or more in investable assets.

SPEAKER_00Aaron Powell Before we get into their findings, we needed to find that word decumulation. It is a term actuaries love to use, but clients never say it.

SPEAKER_01Decumulation is the phase of life where you stop adding money to the bucket and you start draining it to pay for your life. Think of it like flying an airplane. Accumulation is the climb. You are working hard, saving money, gaining altitude. Decumulation is the landing.

SPEAKER_00That is a great way to put it.

SPEAKER_01You are coming down, but you have no idea how long the runway is because you do not know how long you're going to live. It is incredibly stressful.

SPEAKER_00Aaron Powell And the Corebridge study proves exactly how terrifying that landing is for people. What did they find?

SPEAKER_01Aaron Ross Powell 47% of the people surveyed would prefer $60,000 per year guaranteed for life over a $1 million lump sum at age 65. Only 41% actually wanted the lump sum.

SPEAKER_00Aaron Powell Wait, think about that psychology for a second. Almost half the people surveyed would willingly walk away from a million dollars in cold hard cash just to have a guaranteed paycheck they cannot outlive. That tells me they are terrified of the market.

SPEAKER_01Completely.

SPEAKER_00They do not trust their own ability to manage a million dollars without losing it.

SPEAKER_01Aaron Powell They are terrified of running out of money. Only 28% of these pre-retirees and retirees are comfortable drawing down their savings to cover living expenses. A staggering 70% say it is very important their nest egg does not shrink in retirement.

SPEAKER_00I have sat across the kitchen table from these folks for over two decades. Half of them associate retirement spending with uncertainty, and 44% associate it with outright anxiety. When you have a client in your book feeling that kind of anxiety, pitching guaranteed income is not a hard sell.

SPEAKER_01No, not at all.

SPEAKER_00This is your book begging for downside protection. They are literally asking to buy certainty.

SPEAKER_01They want the security, yes. But more importantly, they want permission to spend. Nearly three in four people believe having guaranteed lifetime income would positively impact their ability to spend on things that make them happy.

SPEAKER_00Right. They want to know they can buy a plane ticket to see their grandkids without feeling guilty that they're draining their medical emergency fund.

SPEAKER_01Exactly. Retirees with guaranteed income want to spend more on travel. That is 69% of them. 29% want to spend on home improvements. 25% want to dine out more.

SPEAKER_00I hear all of this, and the data is rock solid. But here is the friction an agent is going to feel. Let us say I am a health agent. I sold Mrs. Smith a Medicare Advantage plan last year. She sees me as the health insurance guy. Why would she trust me with her life savings? How do I pivot from talking about co-pays to talking about half a million dollars in retirement assets?

SPEAKER_01Well, she will trust you because you solved a massive complex problem for her already. You navigated the government bureaucracy of Medicare. You made sure her doctors were in network. You established a baseline of trust that a cold-calling financial advisor simply does not have. You are already inside the circle of trust.

SPEAKER_00That makes sense. The relationship is already there, but you still need a transition script that does not feel like a jarring sales pitch.

SPEAKER_01You do. You need to frame the conversation around what the income enables, not the product mechanics. You talk about the travel and the kitchen remodel, not the participation rates or the cap rates. Here is the exact script I would use on your existing clients this week. I set you up on Medicare last year. I want 20 minutes on one question I did not ask then. If you had to choose between a million dollars cash and $60,000 a year guaranteed for life, which would give you more peace of mind.

SPEAKER_00Man, that approach completely disarms them. You are not asking them to buy an annuity. You are asking a philosophical question about peace of mind. It forces them to articulate their own fear of decumulation out loud.

SPEAKER_01And it immediately shifts the conversation from a financial product to an emotional feeling.

SPEAKER_00Mastering that specific transition is everything. It is the bridge between a $50 health commission and a massive annuity target. If you need to refine your delivery on that, PSM brokerage's verified training services are incredibly valuable here. You can practice these exact guaranteed income transition scripts with professionals until they sound entirely natural and conversational rather than sounding like you were reading off a notepad.

SPEAKER_01So you understand the math of why leads are too expensive, you understand the demand for downside protection, you have the script in hand. Now you need a systematic workflow to execute this across your entire agency. We need to turn this theory into a daily process.

SPEAKER_00Let us look at the sheer scale of the opportunity in your book first. Lyam Ray estimates as many as 100 million Americans live with a life insurance coverage gap. Your clients are a piece of that number. They are sitting in your filing cabinet right now, totally underinsured.

SPEAKER_01And remember, the decumulation fear from the Corbridge study 56% of people regret running out of money while still alive. Only 6% regret dying with money left over. Wow. The fear of going broke is 10 times stronger than the regret of leaving too much behind.

SPEAKER_00Furthermore, half of Generation X respondents, those aged 45 to 55, said guaranteed lifetime income would be highly valuable. This is the aging in wave. This is the demographic that hits your Medicare book over the next 10 years. You have to prospect them right now before someone else does.

SPEAKER_01So here is the exact workflow I would run this week to capture that demand. Pull your entire Medicare client list today. Export it from your CRM. You are going to tag every single client in one of three ways to create targeted segments.

SPEAKER_00Okay, let us break down those three tags. Who are we looking for?

SPEAKER_01First, look for clients over 62 with retirement assets. That group is your primary target for an annuity or an RLA. They are the ones staring down the runway, terrified of the landing. Second, look for clients who are still working.

SPEAKER_00Right, the younger group.

SPEAKER_01Yes, this is the pre-Medicare crowd, the 45 to 55 demographic. That is your target for Index Universal Life and a comprehensive needs analysis. Third, identify your Medicare clients who have adult children. That is your target for life insurance referrals.

SPEAKER_00Tagging them makes the data actionable. I love that. But I have to push back again. Once you have them tagged in your CRM, how are you actually opening the door? You cannot just call the client you have not spoken to in 11 months and abruptly ask if they have a retirement account you can roll over. You will sound like a desperate salesperson.

SPEAKER_01You absolutely cannot do that. You need a seamless entry point that feels like a natural extension of the service you already provide. Here is the exact outreach text or voicemail to use for these tagged clients. Hey Sarah, I do a coverage check on every client once a year. Takes 15 minutes, just making sure nothing changed since last October.

SPEAKER_00That is brilliant. It works precisely because it is just good customer service. You are checking in, it opens the annual review door without any pressure or product pitching.

SPEAKER_01And it positions you as a professional managing their overall risk, not just a Medicare order taker. During that 15-minute coverage check, you ask the million dollar versus $60,000 question. That is how you pivot.

SPEAKER_00Now, if you want to scale this effectively across hundreds of clients, doing this manually is a nightmare. This is where technology has to do the heavy lifting. PSM Brokerage's marketing hub is verified to automate this exact tagging process. You can deploy these annual review campaigns seamlessly to your entire list without manually texting every single person one by one. Yeah, that saves so much time. It triggers the text, and you just take the appointments when they reply.

SPEAKER_01That is the efficiency we were talking about at the beginning. You are not buying new leads, you are automating the extraction of value from the leads you already own.

SPEAKER_00So, what does this all mean for you as an independent agent? As we wrap up today, I want to leave you with a powerful realization. The solution to surging lead costs is not working 80-hour weeks. It is not taking on massive credit card debt to buy live transfers that do not convert.

SPEAKER_01The solution is recognizing the immense value of the assets you already hold in your hand.

SPEAKER_00Exactly. The trust you build selling a zero-dollar premium Medicare plan is the exact same trust needed to protect a half million dollar retirement account. You just need to have a different conversation with the people who already know your name. They are sitting right there in your CRM, terrified of the market, waiting for someone they trust to ask the right question about their peace of mind. Will you be the one to ask it?

SPEAKER_01That is the real question you have to ask yourself tonight.

SPEAKER_00That's this episode of the Insurance Producers Guild. Stay tuned for the next episode. If you're not already with PSM Brokerage, this is the kind of actionable intelligence our agents get. Talk to us about contracting.